Криптовалюты: перспективы, возможность заработка и тп

-

1000+подписчиков

1000+подписчиков

-

ПопулярностьТоп-1

-

Постов+702

-

Просмотров+62510

-

Подписок+2

-

Карма автора0

-

Коль пришлось зайти на форум, не могу не поддержать эту интересную дискуссию и сформулировать свой взгляд на отечественное (и не только) криптоинфополе. Это пост не о личностях, а о криптоконтенте. Он может быть ошибочным и очень субъективный, что уж поделать, говоконтент, как грится:D Впервые зайдя в криптосферу (допустим, сейчас), юзер ищет инфу там, где привык - на ютубе - и наталкивается на тех, с кем боже-упаси встретиться: Кириллом Эвансом и некоторыми другими одноклеточными. Если человек обладает критическим мышлением и догадается, что здесь что-то не так, начнёт копать глубже, то непременно начнёт находить более адекватные источники информации, иначе - тупик, крипта не для него. Критическое мышление при этом, как указал товарищ VANISH, ни в коем случае нельзя терять, поэтому мы всегда должны примерно понимать цель, с которой авторы делают свой контент, ибо цели эти бывают совсем корыстными, а бывают вполне адекватными. Следующий чекпойнт на этом пути - Инкриптед (с блевотными переводами, которые видимо вообще не ебут что и как переводят), с минимумом полезной информации, делающие контент ради контента. Сюда же - дубльтопы, которые сегодня учат фармить в играх, где для заработка 3.5 баксов нужно сделать 10к кликов ЛКМ/сутки, они же завтра поведут вас спекулировать с нфт, а послезавтра выпустят свой нфт с кусочком говна, а через неделю - откроют школу, в которой научат вас делать нфт и заниматься говном. Это контент, который будет съедать всё ваше время (ведь пишут они десятки постов/сутки в тг). Сюда же Топ Трейдерсы, ворующие контент и нещадно банящие в чатиках и так далее. Сюда же белый и пушистый Слёзы Сатоши со своим понци-другом, с его аффилированностью с окекс (патрон антоши, или как там?), с его дрочевом на количество подписоты (реклама, аллокации, т.п., а волку нужно стадо овец), с его зашкварными делишками примерно полутора годами ранее. Ну это всё инстаскип. Если уж хотите погрузиться в эту категорию - погружайтесь в контент инкриптед и слёзы сатоши. Ну и всяких форклогов. Это всё инфлюенсеры первой, очень корыстной категории, которые дадут вам минимум полезного, а с учетом затраченного времени это того не стоит. Если вы желаете добиться цели - копайте дальше. Отдельно про чатики - не сидите в чатиках. Время - ваш самый ценный ресурс. Многотысячные чатики - говно, не вляпайтесь. Запрыгивая в крипту сейчас, вы запрыгиваете во второй, может быть в третий, четвертый, пятый (но не в последний) вагон. Сидите только в чатиках don_eric, там только годнота (тут две ссылки), там сидят такие джипситимовцы как RV, Генр, Gift, GreyPK, которых я очень уважаю (кого не упомянул, того не сдеанонил:)) А ещё наше пари на удвоение ста тыщ баксов в дефи активно, но только не с Сергеем Джипси и его очередью из друзей, а с Эриком (я хотел сэкономить), я всё ещё, увы, не удвоился, поэтому в чатиках публикую отчёты в первое число каждого месяца, вэлком, друзья. Кстати, придется заставлять себя читать, да. Читать каждый день, всё свободное время. Ведь ты хочешь стать компетентным? Копаем дальше и следующий чекпойнт - люди, всё так же могущие мягко шиллить свои сумки, всё так же аффилированные с какими-то платформами, всё так же дающие вам рефки (но открыто, признавая это). Но они дают взамен уже плюс-минус полезный контент. Это и Криптоламер (ещё и ещё), аффилированный с 3комманс, компонентом и много с чем ещё, но делающий очень няшные ютуб-видео, это и Заводил, связанный с нир протоколом. Это Якудза с их "С нуля до нуля на крипте", тоже делающие годный контент. Это хорошо, они молодцы. Есть ещё сумасшедший заговорщик китобой, есть биткоин-макси Bitcoin Translated. Сюда же (или следующий чекпойнт?) следует добавить тех, чья выгода от ведения каналов не очень понятна (помимо расширения аудитории) или совсем минимальная - Крипто Аналитик, Дефискамчек. И мой горячо любимый Базовый блок. Тут вам минимум буллщита и подобного говна. У ББ - довольно сложный, технический контент, слушать-не переслушать, но это очень интересно, это, возможно, изменит ваш взгляд на происходящее. Не бойтесь сложностей и просто слушайте. И вы вдруг поймёте, что вы здесь за технологию, а не ссаный спекулянт:) Ну а далее всё уже просто - вы заводите аккаунт в твиттере и тут вам открывается настоящая кладезь. Вы подписываетесь на узкий список самых главных действующих лиц (топ-шиллеров), а дальше сам твиттер проведет вас за руку сквозь дебри аккаунтов и покажет на кого стоит подписываться (топ-ресерчеров). Вы можете создавать списки, это очень удобно. И если у вас несколько мониторов, один можете занять твитдеском, в котором организуете твиттер так, как вам удобно. Также неоценимую помощь в организации вашего рабочего пространства и систематизации знаний сыграют ношн и обсидиан. (Не спешите скипать эту инфу, эти две вещи сыграли важнейшую роль в моей самоорганизации, разберитесь). В итоге вы будете получать в ленте твиттера самые годные треды, вы будете получать инфу из первых рук. Вы сможете ресёрчить проекты одним кликом - перейдя из коингекко по вкладке "твиттер" и видя, кто из тех, за кем вы следите, подписался на проект. Дальше вы, может быть, оформите подписку на медиуме за пять долларов/месяц, подпишитесь на Hasu и прочих, будете получать обновления о новых статьях на емейл и читать их. Дальше вы непременно подпишетесь на новостные рассылки всяких банклесс (хоть они тоже те ещё эфир-макси и шиллеры), подпишитесь на годноту от Энтони Сассано, на дефиант , на всякие йелдфермер, начнёте читать статьи гласснод. Начнёте смотреть на ютубе годноту, например лекции кибер академии, где вам объяснят лучше меня почему стейбл даи - хорошо, а стейбл айрон - говно. Будете читать лучший ру_форум о крипте. Может быть, вы заинтересуетесь ресёрчем и подпишитесь на мессари и дельфидиджитал. Если для вас это дорого, не беда - можете убить одним выстрелом двух зайцев задёшево (там 99% - шлак, не обольщайтесь). Быть может, вы заинтересуетесь он-чейн аналитикой на том же глассноде, а может вам понравится нансен или вы откроете для себя все грани дюнаналитикс. Быть может, вы начнёте следить за фондами, за всякими лысыми дядьками. Но это возможно

+314

-

Биткоины это просто. Очень просто Биткоины - это криптовалюта, которая позволяет быстро и дёшево переводить "деньги" между пользователями интернета. Криптовалюта означает, что эту "валюту" никто не контролирует и никто не регулирует, она просто сама по себе живёт в интернете в виде алгоритмов и программ, которые этими алгоритмами пользуются. Стоимость криптовалюты определяется рынком, например сейчас, в конце февраля 2017 года, биткоин стоит в районе 1150$, а в феврале 2016 года стоил 350$, в 2015 цена была 220$, а в феврале 2014 цена была 800$. Очень удобно смотреть движения курсов по различным биржам/валютам (в том числе текущий "правильный" курс) на сервисе bitcoinwisdom. Как видите, цена в прошлом очень сильно колебалась, то взлетала до небес, то падала резко и быстро. Я предполагаю, что подобная волатильность уже в прошлом, биткоин повзрослел, всё больше и больше людей и компаний пользуются им и строят на нём свою инфраструктуру платежей, а значит курс будет определяться всё большей денежной массой, что придаст ему определенной устойчивости. Я не могу дать совет, стоит ли покупать биткоин в спекулятивных целях (купить сейчас по 1200, чтобы потом продать по 2000), но скажу, что любая спекуляция требует знания предмета спекуляции, иначе она заканчивается быстро и плачевно. В этой статье я опишу, как просто, безопасно и эффективно использовать биткоины для платежей прямо сейчас. Статья расчитана на начинающих пользователя, многие моменты опущены и упрощены, главное - чтобы вы смогли без особых хлопот приобщиться к сообществу пользователей криптовалюты, а дальше разберётесь сами, если сильно захочется. Будут приведены примеры, как лучше всего работать с биткоинами в России и Евросоюзе, про остальные локации я не знаю даже понаслышке, но скорее всего алгоритм действий будет схожим. Создание собственного кошелька На самом деле этот этап необязательный, потому что потом биткоины нужно будет где-то покупать (менять на "фиат", так называются "обычные деньги", доллары, рубли, евро), а любые сервисы по обмену создадут вам свой кошелёк. Некоторые предпочитают держать деньги на счету биржи / сервиса по обмену и с него уже рассылать по мере надобности. Однако это методически неверно, поэтому мы создадим собственный кошелёк. Всего лишь нужно перейти по адресу https://bitcoin.org/ru/choose-your-wallet и выбрать кошелёк, который вам нравится больше, дальше следовать инструкциям сервисов, разберётесь самостоятельно, там всё просто и доходчиво. Если выбирать лень - используйте Copay для платежей через компьютер (в виде приложения для браузера на основе Chromium, это Яндекс.Браузер, Гугль Хром, тысячи их) и iOS. Для Android очень хвалят MyCelium за удобство, ну а если эти два не понравились - попробуйте Electrum Некоторые кошельки предоставляют услугу "ротации используемых адресов". Это означает, что программа будет постоянно менять номера ваших кошельков, чтобы затруднить слежение за вашими транзакциями. Я смысла в этой новомодной приблуде не вижу (ну кому интересны лично ваши транзакции, а даже если и интересны - что ценного можно из них почерпнуть, вы же не наркотики/оружие покупаете в Darknet, а всего лишь хотите полудить в покерруме/казино/букмекерской конторе на биткоины) и поэтому стараюсь использовать один кошелёк, но это скорее вопрос привычки. Итак, теперь у вас в любой момент времени есть ваш личный адрес, на который вы можете получить биткоины (хотя без него можно обойтись, используя адреса бирж и обменников). Покупка/продажа биткоинов На самом деле, когда мы говорим покупка/продажа биткоинов, то подразумеваем их обмен на "фиат", реальные деньги. Способов этого обмена великое множество, и все отличаются по эффективности (сколько комиссий нужно будет заплатить), удобстве (насколько сложно провести операцию обмена) и безопасности (насколько велика вероятность, что вас обманут при обмене). Оптимальный способ зависит от того, каким "фиатом" вы располагаете и к каким банковским инструментам имеете доступ. Процесс продажи биткоинов и выводу их обратно в наличные деньги полностью аналогичен процессу покупки, тут нет никаких подводных камней. Рубль, российские банки Здесь единственный вменяемый вариант - обратиться к меняле. Для этого я исключительно рекомендую сервис localbitcoins. Нужно зарегистрироваться, выбрать быстрая покупка, город вводить не надо, только страну "Россия" (ну или другую, попробуете). В итоге выйдет список предложений с методами платежа, который принимает меняла и его ценой. Особенной популярностью пользуются банки Альфа-банк (услуга CASH-IN которая позволяет пополнять чужой счёт наличными без идентификации, просто по номеру) и Тинькофф (очень удобный интернет-банк), я очень советую вам открыться хотя бы в одном из них, очень полезно для всяких обменов и переводов. Рассмотрим, как купить биткоины (все действия при продаже аналогичны). Вы выбираете с кем меняться (рейтинг должен быть 100% и хотя бы полсотни операций проведено), отправляете запрос на сделку. После принятия этой сделки, localbitcoins блокирует у продавца биткоины, на сумму сделки. После этого все ждут, пока вы переведёте продавцу деньги, он подтверждает получение, localbitcoins переводит биткоины на ваш счёт, откуда их можно вывести на ваш личный кошелёк или сразу отправить куда-нибудь ещё. Если по каким-то причинам продавец откажется подтверждать факт получения от вас денег - вы просто создаёте жалобу, прикладываете подтверждения совершенного платежа, её достаточно быстро рассматривают и вы всё равно получаете свои биткоины, всё просто и удобно. Если вам не нравится localbitcoins - попробуйте поискать менялу на мониторинге обменников bestchange, но там уже вы будете меняться напрямую, без какой-либо защиты, впрочем вероятность, что на мониторинге будут мошенники достаточно низка. Если вам вообще ничего не нравится - откройтесь на одной из биткоин-бирж, работающих с рублём, вот вам три самых приличных: BTC-e, EXMO и Livecoin. Чтобы воспользоваться ими нужно будет перевести им рубли, скорее всего придётся это сделать с помощью какой-нибудь платёжной системы (например Qiwi или Яндекс-деньги), а для этого нужно будет разобраться, как пополнить саму платёжную систему, в общем этот способ посложнее. Но если вы оперируете крупными суммами - он самый правильный, так как позволяет максимально снизить потери при конвертации рублей в биткоины. Евро, счёт SEPA в банке евросоюза Если вам посчастливилось каким-то образом стать обладателем счёта SEPA, то всё вообще просто и удобно, открываетесь на самой ликвидной бирже для пары EUR/BTC, которая называется kraken, отправляете на неё евры SEPA-переводом, через пару часов они приходят, вы их меняете по рыночному курсу и всё, можно забирать биткоины. Азартные игры на биткоины В силу своей нерегулируемости, биткоин очень-очень подходит для зарегулированного донельзя рынка азартных игр в интернете. Есть казино, есть букмекерские конторы, даже в покер поиграть можно на биткоины. Вот здесь уважаемый буржуйский сайт рейтинг букмекеров собрал обзоры принимающих биткоины, можно ознакомиться. Лучший из чистых биткоин-проектов, с казино, покером и букмекером - это NitrogenSports, можно с него начать своё знакомство. Ну и, конечно, биткоины можно посылать друзьям, на них можно спекулировать, ими можно оплачивать всякие покупки, с каждым днём всё больше мест принимают биткоин, это больше не экзотика, а достаточно распространенный вариант. Безопасность средств на биткоин-кошельке Вообще, конечно, определенный риск, что злоумышленники получат доступ к вашему биткоин-кошельку, имеется. Но он не больше, чем риск потерять контроль над почтовым ящиком или аккаунтом во вконтактике. Поэтому, на мой взгляд, никаких особенных мер защиты для того, чтобы начать пользоваться биткоинами, предпринимать, поначалу, не следует. Потом, когда во всём разберётесь, можно уже заморачиваться по поводу "бумажных кошельков", "железных" кошельков типа Trezor, bitcoin-mixer'ами и прочими продвинутыми штуками. Для начала же более чем достаточно внимательно читать инструкции на сайтах разработчиков кошельков / бирж обмена и следовать им, там обычно всё вменяемо написано. Вместо заключения Цель этой статьи - помочь вам приобрести (и потратить) свои первые биткоины, показать, что время настало, пользоваться криптовалютой можно и нужно уже сегодня, это дёшево и удобно. Очень, очень многие вопросы не освещены здесь - что такое miner fee и зачем она нужна, как сохранить копию своего кошелька, чтобы не зависеть от программы, в которой он сгенерирован, как с умом настроить удобную двухфакторную аутентификацию для пущей безопасности, как и где оформить привязанную к биткоинам пластиковую карту и расплачиваться криптовалютой в продуктовом магазине, всего не перечислить. При должном желании эту информацию не так уж сложно найти в интернете, но если будет сильная потребность у уважаемых читателей - я могу написать ещё несколько подобных инструкций на тему компьютерной финансовой безопасности вообще и криптовалют в частности. Оригинал тут. Я старался, чтобы получилось попроще, проще, наверное, некуда, вы пишите, если что-то нужно улучшить, где-то непонятно, можно в тему, можно в личку, как вам удобнее, лучше в тему, конечно.

+226

-

Самое страшное, что если крипта упадёт ещё ниже, то придётся начать играть в покер.

+224

-

ChillLEO, семена капусты

+219

-

Парни, помогите выиграть конкурс гифок на криптотему, если моя займёт первое место - переведу 3им плюсанувшим пост и проголосовавщим за моё творение по 50$. Под спойлером гифка и сайт где проводится конкурс. https://experty.io/gif-competition Она должна быть где-то в 1-х 4-х рядах сверху. П.С. В ваших же интересах не просто плюсануть пост, но и проголосовать на сайте.

+203

-

-

А это может быть издержками "нерегулироемости" ? Или на классическом тоже самое?

-

tester37, на регулируемом плюс-минус тоже самое, просто в силу намного большего объема ликвидности там проще окешить свои позиции, не обрушив рынок (ОТС тоже куда проще найти). Плюс обеспеченность позиций (например, акции те же так или иначе подкреплены прибылью/имуществом компаний, долю в которых они отражают).

Кризис недвижимости США 2008 года был чем-то подобным. Тогда тоже было так, что цена на недвигу летела в небо, все её покупали в кредит (кредиты давали на раз-два, т.к. банки их все равно потом упаковывали в группы и продавали инвесторам, как бумаги с надежностью ААА) под залог самой недвиги. Накредитованными бабками раздули ценник на недвижку. Пока в один момент ценник не начал падать, народу стало выгоднее перестать платить кредит и отдать эту недвигу кредитору, чем выплачивать кредит за неё (дом стал стоить 150к$, а покупался за 250к$, из которых выплачено всего 10к$). Кредиторам надо эту недвигу продать, но из-за их предложений цены на недвигу еще больше падают. От этого еще больше заемщиков перестают платить и т.д. по цепочке. То есть тогда в роли крупного игрока выступили американские семьи, которые, пользуясь легким получением ипотеки, раздули цену на недвигу. А ликвидности у них не было.

-

Меня смущает полпроцентный депег USDT, вот никогда не напрягала тема с тезором а сейчас почему-то тревожит. Сизый захочет рано или поздно подмять под свой BUSD всё остальное.

-

mihhhhey,

Кажется, что если грохнется USDT, именно сейчас, то гг вся крипта, если не навсегда, то на очень долгие годы... скорее всего, он мало заинтересован в таком исходе

А вот в будущем, если разгонит BUSD, и USDT будет терять популярность, такой исход станет более вероятным

-

10-минутное чтиво про FTX, залоги и т.д. от Блумберг на англ

Bloomberg

FTX

So how could this happen? I don’t know, but let me speculate a little bit.Let’s start with Coinbase. Coinbase Global Inc. runs a cryptocurrency exchange. When FTX.com, one of the largest crypto exchanges, was instantaneously vaporized yesterday, Coinbase put out a statement, the gist of which was “don’t worry, we are not going to be instantaneously vaporized.” The part that I want to focus on is this paragraph:

There can’t be a “run on the bank” at Coinbase. As you can review in our publicly filed, audited financial statements, we hold customer assets 1:1. Any institutional lending activity at Coinbase is at the discretion of the customer and backed by collateral. We have no gating for client loan recalls or withdrawals.

The way it works is roughly that you open an account and send dollars to Coinbase, and then you tell Coinbase “I’d like to buy some Bitcoin with those dollars,” and Coinbase buys Bitcoin and holds on to it for you and charges you a fee for that transaction. You can check your account balance, and Coinbase says “you have 0.5 Bitcoin” or whatever. That 0.5 Bitcoin is, in the general case, held by Coinbase; it has possession of the Bitcoin.[1] But it is held in a custody account for you. Coinbase says:

Your funds are your funds, and your crypto is your crypto: Coinbase maintains internal systems, like a bank or a broker. Our fully audited ledger identifies your account, your fiat and crypto holdings, and tracks your account activity in real time. There’s never a situation where customer funds could be confused with corporate assets.

We will never repurpose your funds: We do not lend or take any action with your assets, unless you specifically instruct us to. Many banks and financial institutions use customer funds for commercial purposes including lending and trading, meaning that they often hold only a fraction of their customer assets at any given time. Coinbase always holds customer assets 1:1. This means that funds are available to our customers 24 hours a day, 7 days a week, 365 days of the year.

The analogy is: Imagine a weird sort of bank. You come to the bank with $100 in paper bills, and you deposit it in the bank, and the bank takes your paper bills and sticks them in an envelope with your name on it. Then it sticks the envelope in a vault, and if at any point you ask for your money back, it opens the vault and hands you your envelope. This sounds like a bad business model: The bank needs to pay for real estate and tellers and vaults, and it is not doing anything with your money. But the other weird thing about this bank is that, every day, you come in and say “hey I’d like to exchange my dollars for euros” or “my euros for pounds” or whatever, and each time you do that the bank charges you a dollar. So you have $100, which you exchange for €99, which you exchange for £98, which you exchange for $97, etc.,[2] paying the bank $1 each time. If all of the bank’s customers do this every day, then the bank makes plenty of money to pay for real estate and tellers and vaults and executive bonuses, without doing anything else with your money. It just takes the $100 out of your envelope and replaces it with €99, etc., always keeping exactly the right amount of money (in whatever currency you like that day) in exactly your envelope.[3]

And then if one day every single customer walked into the bank at the same time and said “we would like our money back,” the bank would just hand them all their envelopes. Don’t get me wrong, this would be a catastrophe for the bank: If everyone took their envelopes back, then presumably they would stop changing money at the bank and paying fees, and the bank would stop making money, and it would no longer be able to pay for real estate or tellers or vaults or executive bonuses. It would go out of business in fairly short order. But it would not go out of business that minute. It would actually have enough money to give all the customers their money back, because it kept all the customers’ money in their own envelopes the whole time.

No actual bank works that way. Real banks take deposits but don’t keep the money in envelopes; they lend it out.[4] Most classically, they borrow short to lend long, taking checking deposits that can be withdrawn at any time, and using them to make long-term mortgages. This makes them vulnerable to runs, Diamond-Dybvig, It’s a Wonderful Life, etc., everyone knows all this.

But in theory a cryptocurrency exchange could work that way, and at a high level of generality Coinbase sort of does.[5] Historically — not so much now, but until early this year anyway — cryptocurrencies were volatile and exciting and people were jazzed to trade them a lot, so you could make a lot of money by just charging fees without doing anything else with customer assets. And that is a run-proof business. If everyone takes their money out at once, you have the money.

But then one day a customer comes to you and says “I have $10,000, but I am really bullish on Bitcoin, so I would like to buy $20,000 worth of Bitcoin. Why don’t you lend me $10,000 so I can buy $20,000 of Bitcoin, so I can get more excitement?” This is called a margin loan.

Or — equivalently — a customer comes to you and says “I have $20,000 of Bitcoin in my account, and I need some cash this month. I don’t want to sell my Bitcoin, because I am a true believer and also do not want to realize gains for tax purposes. Could you just lend me $10,000, secured by my $20,000 of Bitcoin? You know I’m good for it: If I don’t pay you back, you can sell my Bitcoin and pay yourself back from the proceeds.”

You might just say “no, that’s dumb, Bitcoin is volatile, buying $10,000 of Bitcoin is plenty of excitement.” (In fact Coinbase shut down margin trading in 2020.) But your competitors probably offer loans, and it is tempting for you to do it too. So you say, sure, fine, I’ll take your $10,000 and put $20,000 of Bitcoin in your account.

But where do you get the money that you are lending to the customer? Well, you have to borrow it too. Ordinarily the way that you will borrow it is by putting up the customer’s Bitcoin as collateral to your lender, just as the customer puts up its Bitcoin as collateral to you. If the customer defaults, you still have to pay your lender (and then you get the Bitcoin back and can sell it to pay off your customer’s liability to you); if you default, the lender sells the Bitcoin.

But who are the lenders? Oh, various possibilities. But one general point is that while some customers will want to borrow dollars to buy Bitcoin, other customers will want to borrow Bitcoin. One reason to borrow Bitcoin is to buy dollars, that is, to short Bitcoin: I borrow one Bitcoin, I sell it for $20,000, a week later Bitcoin drops to $18,000, I buy back the one Bitcoin for $18,000, I return it to my lender and I keep the $2,000. There are variations on this trade (I borrow Bitcoin and sell it for Ethereum, betting on the relative value between the tokens, etc.). It is necessarily a leveraged trade; I can’t short Bitcoin without borrowing it.[6]

If you are a crypto exchange, this is a nice opportunity. You have Customer A who has Bitcoin and wants to borrow dollars, and Customer B who has dollars and wants to borrow Bitcoin. (By “dollars,” for a crypto exchange, I mostly mean “dollar-denominated stablecoins,” though potentially also dollars.) You take some of Customer A’s Bitcoin and lend it to Customer B, and you take some of Customer B’s dollars and lend them to Customer A. Each of them is overcollateralized — you only lend Customer A half the value of her Bitcoin, and you only lend Customer B half the value of his dollars — so you feel pretty safe. And they both pay you interest.

But there are risks. One day Customer A might come in, pay off her dollar loan, and ask to take her Bitcoin back. You don’t have her Bitcoin, or not all of them anyway; some of them are with Customer B. Customer B owes them to you — ultimately you’re good for it — but you don’t have them now. There is a timing problem.

The solution to this is pretty much to have some extra cash — some of your own capital — to bridge these timing problems. Eventually you’ll get the rest of the Bitcoin back from Customer B, but for now you just pay Customer A out of your own Bitcoin stash.

But the timing problem is also connected to a real economic risk. If the price of Bitcoin falls by 90%, Customer B will be thrilled. He will come to you and say “here’s my Bitcoin back, I’d like to withdraw my dollars.” But you don’t have his dollars, or not all of them; half of them are with Customer A. Your dollar loan to Customer A is now underwater: You loaned her 50% of the value of her Bitcoin, but Bitcoin fell by 90%, so she owes you more than her collateral is worth. You call her up and ask her for more money — a “margin call” — but she, sensibly, doesn’t answer the phone.[7] You have to pay Customer B out of your own capital, and you don’t get it back from Customer A. You've just lost money. Actually that’s the best outcome. The worst outcome is that you don’t have enough capital, you go bankrupt, and Customer B does not get his money back.

Everyone knows this, which is why crypto exchanges — and securities broker-dealers, who have the same basic business model — spend most of their time thinking about risk management. Before the price of Bitcoin drops too far, you will be calling up Customer A for more margin, and if she doesn’t answer the phone you will liquidate her position to pay back the loan you made. If you are a sophisticated modern crypto exchange like FTX, you will have automated 24/7 margining systems that automatically liquidate trades that have gotten too risky, so that only the rarest catastrophic market moves could get you in trouble.

But sometimes market moves are catastrophic, and in particular, sometimes securities broker-dealers and crypto exchanges will have “run on the bank” risks. If everyone knows that you are in this situation — that you have a lot of Bitcoin collateral and Bitcoin prices are falling — people will expect you to have to liquidate your Bitcoin collateral, so they will expect Bitcoin prices to fall, so they will sell Bitcoin, which will cause Bitcoin prices to fall, which will cause your long-Bitcoin customers to default, which will cause you to liquidate Bitcoin at lower and lower prices, etc., until you are bankrupt.

Now let’s add one more crypto element. If you are a crypto exchange, you might issue your own crypto token. FTX issues a token called FTT. The attributes of this token are, like, it entitles you to some discounts and stuff, but the main attribute is that FTX periodically uses a portion of its profits to buy back FTT tokens. This makes FTT kind of like stock in FTX: The higher FTX’s profits are, the higher the price of FTT will be.[8] It is not actually stock in FTX — in fact FTX is a company and has stock and venture capitalists bought it, etc. — but it is a lot like stock in FTX. FTT is a bet on FTX’s future profits.

But it is also a crypto token, which means that a customer can come to you and post $100 worth of FTT as collateral and borrow $50 worth of Bitcoin, or dollars, or whatever, against that collateral, just as they would with any other token. Or something; you might set the margin requirements higher or lower, letting customers borrow 25% or 50% or 95% of the value of their FTT token collateral.

If you think of the token as “more or less stock,” and you think of a crypto exchange as a securities broker-dealer, this is completely insane. If you go to an investment bank and say “lend me $1 billion, and I will post $2 billion of your stock as collateral,” you are messing with very dark magic and they will say no.[9] The problem with this is that it is wrong-way risk. (It is also, at least sometimes, illegal.) If people start to worry about the investment bank’s financial health, its stock will go down, which means that its collateral will be less valuable, which means that its financial health will get worse, which means that its stock will go down, etc. It is a death spiral. In general it should not be possible to bankrupt an investment bank by shorting its stock. If one of the bank’s main assets is its own stock — is a leveraged bet on its own stock — then it is easy to bankrupt it by shorting its stock.

The worst case is something like:

You have 100 Customer As who are long Bitcoin on margin: They each have 1 Bitcoin in their accounts and owe you $10,000.

You have 100 Customer Bs who are short Bitcoin on margin: They each have $20,000 in their account and owe you 0.5 Bitcoin.

You have loaned 50 of the Customer As’ Bitcoins to the Customer Bs, and $1 million of the Customer Bs’ dollars to the Customer As. You keep the other 50 Bitcoins and $1 million as collateral.

Your accounts show that you owe clients 100 Bitcoins and $2 million, and that they owe you back 50 Bitcoins and $1 million, and you have 50 Bitcoins and $1 million on hand, so everything balances.

You have one Customer C who says “hi I would like to borrow 50 Bitcoins and $1 million, I will secure that loan with 150,000 FTT, each of which is worth $20.”

You say “sure, sounds good,” and hand over all your collateral.

Now you have 150,000 of FTT, worth $3 million, as collateral (and no Bitcoins or dollars).

Your accounts show that you owe clients 100 Bitcoins and $2 million and 150,000 FTT, and they owe you back 100 Bitcoins and $2 million, and you have 150,000 FTT of collateral, so everything balances.

But then if the value of FTT drops to zero, you have nothing. You have no Bitcoins to give to the customers to whom you owe Bitcoins, no dollars to give to the customers to whom you owe dollars. You just have to call up Customer C and say “hey we need all those dollars and Bitcoins back.” But Customer C will not want to give you back all those valuable dollars and Bitcoins in exchange for now-worthless FTT. Also the fact that Customer C had all that FTT in the first place is not a great sign. It is an FTT whale, and FTT is now worthless. Has it been borrowing elsewhere against FTT? Are all those debts coming due?Now let’s add a few more FTX-specific elements. One is that FTX is an exchange for levered traders, offering products like perpetual futures and leveraged tokens that build in margin lending. So whereas the basic model of Coinbase is “they buy Bitcoin for you and put it in an envelope,” the basic model of FTX has to be “they lend you money to buy crypto and then make use of your crypto to get the money.” In financial terms, they have to rehypothecate your collateral; you can’t expect them to just keep it in an envelope if they’re lending you the money to buy it.

The other is that FTX is closely associated with a hedge fund called Alameda Research. Sam Bankman-Fried founded Alameda to do crypto arbitrage and market-making trades, and then he founded FTX to basically have a better exchange for Alameda to trade on. Alameda has lots of FTT, and last week Coindesk reported on its balance sheet; the gist of that report was “wow its balance sheet is mostly FTT”:

The financials make concrete what industry-watchers already suspect: Alameda is big. As of June 30, the company’s assets amounted to $14.6 billion. Its single biggest asset: $3.66 billion of “unlocked FTT.” The third-largest entry on the assets side of the accounting ledger? A $2.16 billion pile of “FTT collateral.”

There are more FTX tokens among its $8 billion of liabilities: $292 million of “locked FTT.” (The liabilities are dominated by $7.4 billion of loans.)

That is not in itself a reason for a run on FTX! It might be a reason for the price of FTT to go down, if you think that Alameda has too much of it and might need to sell it.

The reason for a run on FTX is that you think that Alameda is, in my terminology, Customer C. The reason for a run on FTX is if you think that FTX loaned Alameda a bunch of customer assets and got back FTT in exchange. If that’s the case, then a crash in the price of FTT will destabilize FTX. If you’re worried about that, you should take your money out of FTX before the crash. If everyone is worried about that, they will all take their money out of FTX. But FTX doesn’t have their money; it has FTT, and a loan to Alameda. If they all take their money out, that’s a bank run.

And all of this is self-fulfilling: If you are worried about FTX’s business, then the price of FTT should go down. If the price of FTT goes down, then FTX’s business is riskier, because it has less collateral. If, say, the operator of the biggest crypto exchange gently raises one eyebrow and says “FTT, eh?” that can be enough to topple FTX. FTT goes down, leaving FTX undercapitalized, leading to customer withdrawals, leading to ruin.

Anyway it is still early and confusing but that seems to be the story of FTX. Coindesk reported on Alameda’s FTT exposure, and then Changpeng “CZ” Zhao, the founder of Binance Holdings Ltd., the largest crypto exchange, raised eyebrows by tweeting that Binance would sell its FTT holdings “due to recent revelations.” People worried that this would tank the price of FTT and put pressure on FTX, so they started withdrawing money from FTX. FTX didn’t have the money, and Bankman-Fried started calling around asking for a loan or a bailout. Eventually he called CZ himself, and they announced a non-binding letter of intent for Binance to acquire FTX and make customers whole. Bankman-Fried’s fortune basically vanished, as did his “ emperor aura.” Venture capital investors in FTX — which last raised money at a $32 billion valuation — are probably getting zeroed, the price of FTT collapsed, and now regulators are investigating.

In this description I have drawn on Twitter threads from Jon Wu, Lucas Nuzzi and an anonymous “Wassie Lawyer,” who make arguments along these lines, as well as this Substack post from Byrne Hobart. But the most informed view is probably that of CZ himself, who tweeted this morning:

Two big lessons:

1: Never use a token you created as collateral.

2: Don’t borrow if you run a crypto business. Don't use capital "efficiently". Have a large reserve.

Binance has never used BNB for collateral, and we have never taken on debt.

“Never use a token you created as collateral” suggests, to me, that FTX accepted its FTT token as collateral, probably from Alameda, probably in exchange for borrowing assets that it owes to customers. And that that went wrong in roughly the way I have outlined.

One other point here is that if this is the story, then it is not a liquidity crisis but a solvency one. That is, the problem is not a timing mismatch, in which FTX’s customers asked for their cash back but FTX did not have enough ready cash because it had long-term but money-good loans out. The problem is that FTX took its customers’ money and traded it for a pile of magic beans, and now the beans are worthless and there’s a huge hole in the balance sheet. On that note:

Changpeng Zhao moved fast when Sam Bankman-Fried’s FTX.com was on the brink, offering to take it over and stem any further crypto contagion.

Within hours, he was forced to reconsider.

For starters, Binance executives quickly found themselves staring into a financial black hole -- a gap between liabilities and assets at FTX that’s probably in the billions, and possibly more than $6 billion, according to a person familiar with the matter.

On top of that, US regulators are circling FTX, investigating whether the firm properly handled customer funds, as well as its relationship with other parts of Bankman-Fried’s crypto empire, Bloomberg News reported Wednesday.

It makes for a tricky decision for Zhao, known in the crypto world as CZ: Follow through with rescuing his onetime top rival and shoulder the financial and regulatory burdens, or let FTX crumble and sort through the potential wreckage? Zhao himself admits there was no “master plan” to take over FTX.

His answer, at least for now, is that the financial hole appears too deep. Binance is unlikely to follow through on its takeover of FTX, according to the person familiar, who wasn’t authorized to publicly discuss the matter.

Seems bad.

-

NightStorm @ 10.11.22

mihhhhey,

Кажется, что если грохнется USDT, именно сейчас, то гг вся крипта, если не навсегда, то на очень долгие годы... скорее всего, он мало заинтересован в таком исходе

А вот в будущем, если разгонит BUSD, и USDT будет терять популярность, такой исход станет более вероятным

Не знаю, по-моему так это эффективное сбривание тех, кто сидит в тезере и ждёт хороших цен для закупа. А биток от такого только пропампится, потому что будут пытаться хоть что-то спасти, переводя тезер собственно в крипту.

-

Тут подумалось, как можно назвать подобную ситуацию: "Миллиардеры Шредингера". Пока кредиторы не просят с них своих бабки – они миллиардеры, а когда начинают просить – они банкроты.

Я только во всей этой ситуации не понимаю вот чего: SBF сам дрючил рынок подобными выкрутасами (с USDN, LUNA, Celsius'ом и 3AC), зарабатывая на этом, его фонд Alameda вообще известен, как самые грязные флиперы, которые сливают свои инвестиции в проекты при первых же анлоках и рушат рынок (и даже еще раньше, открывая шорты еще до анлоков на своей карманной FTX), с одной Соланы они вынесли огромное количество бабла, сама FTX приносила неплохие деньги за счет комиссий и еще временами "подозрительно лагала", обогащая столь же сомнительных крупных игроков, она по-прежнему стоит хороших денег (софт, бренд, в раскрутку которого вложено куча бабла, клиентская база)... Это уже было остейбленное и окешенное бабло. Много бабла. Куда всё оно делось?

-

Мда, уже 2% анпег. Кстати вроде ж как раз на фтп можно было хеджировать фьючами тезер к баксу?

-

NickV, мне кажется ответ довольно очевиден, этим же дядям в карманы)

-

-

NickV, Очень хорошо объясняешь

-

NickV @ 10.11.22

Я только во всей этой ситуации не понимаю вот чего: SBF сам дрючил рынок подобными выкрутасами (с USDN, LUNA, Celsius'ом и 3AC), зарабатывая на этом, его фонд Alameda вообще известен, как самые грязные флиперы, которые сливают свои инвестиции в проекты при первых же анлоках и рушат рынок (и даже еще раньше, открывая шорты еще до анлоков на своей карманной FTX), с одной Соланы они вынесли огромное количество бабла, сама FTX приносила неплохие деньги за счет комиссий и еще временами "подозрительно лагала", обогащая столь же сомнительных крупных игроков, она по-прежнему стоит хороших денег (софт, бренд, в раскрутку которого вложено куча бабла, клиентская база)... Это уже было остейбленное и окешенное бабло. Много бабла. Куда всё оно делось?

Сэм довольно уверенно себя чувствовал в высшем американском управленческом (по финсектору) свете. Ему же за это тоже предъявляли коллеги. Вряд ли эта уверенность объяснялась его харизмой. Слитие странно совпало с выборами.

-

возобновились выводы с фтх, но в малом количестве

-

пишут инфу, что выводят только институциональным инвесторам

когда будут выводить работягам с завода неизвестно

состою в чатике на 2к людей - пока еще никому не вывели

-

-

Friend_, можете пояснить, в чем надо хранить, если не тезер, интересуют именно стейблы, между румами туда сюда гоняю.

-

Exclusive @ 10.11.22

Friend_, можете пояснить, в чем надо хранить, если не тезер, интересуют именно стейблы, между румами туда сюда гоняю.

как вариант в равных пропорциях раскидать между USDT-USDC-BUSD-DAI (сам правда в юсдт сижу))))

ну и конечно хранить только на своих кошельках

вообще депег тезера напряжная штука - сегодня менял юсдт на юсд, повезло, что менялам было пофиг на депег и меняли 1к1 (по факту там расхождении было 2-2,5%)

-

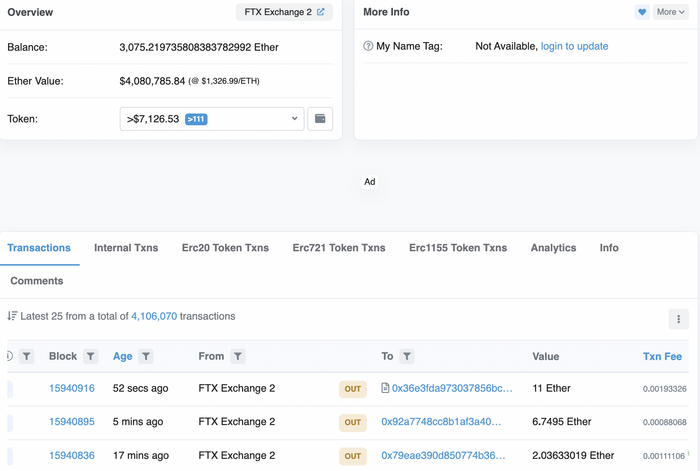

https://etherscan.io/address/0xffbc8bab151a70f3ea92b283ea8890b98e0d6e2f

вот на этот адрес недавно пришел вывод с фтх

похоже все-таки обычным работягам делают выводы

-

1-2% это не дпег, просто у биржи ликвы не хватило покрыть спрос

- Вы сможете оставлять комментарии, оценивать посты, участвовать в дискуссиях и повышать свой уровень игры.

- Если вы предпочитаете четырехцветную колоду и хотите отключить анимацию аватаров, эти возможности будут в настройках профиля.

- Вам станут доступны закладки, бекинг и другие удобные инструменты сайта.

- На каждой странице будет видно, где появились новые посты и комментарии.

- Если вы зарегистрированы в покер-румах через GipsyTeam, вы получите статистику рейка, бонусные очки для покупок в магазине, эксклюзивные акции и расширенную поддержку.

Цена очень чуткая на крипторынке. Даже самое незначительное изменение спроса-предложения отражаются очень существенно на цене.

сброс-покупка 1% эмиссии монеты может толкнуть её цену на десятки процентов. +"Страх-жадность" участников торгов в разы усиливают "эластичность" цены. Если происходит что-то очень значимое для всей криптоиндустрии, то падают-взлетают почти все монеты. Капитализация крипторынка - как воздушный шар, который изменяется непропорционально. Спустили литр воздуха, объем шара уменьшился на сто литров. Вдули лярд капа скакнула на двести)

Как-то так